The United Kingdom produces world-class early-stage technology companies at an astonishing rate. Driven by elite academic institutions in Oxford and Cambridge, as well as a massive concentration of talent in London, the British artificial intelligence ecosystem is undeniably vibrant. The government frequently touts the nation as a global AI superpower.

Yet a severe structural flaw exists within the British venture capital machine. While early-stage seed funding is abundant, the domestic ecosystem utterly fails to support these companies when they attempt to transition from promising prototypes to global commercial scale. The UK has accidentally built the most efficient technology incubator in Europe, only to hand the resulting mature assets over to foreign investors.

To understand this dynamic, we must examine the stark difference between the research and development phase and the brutal reality of late-stage venture capital.

The Data Behind the Incubator Economy

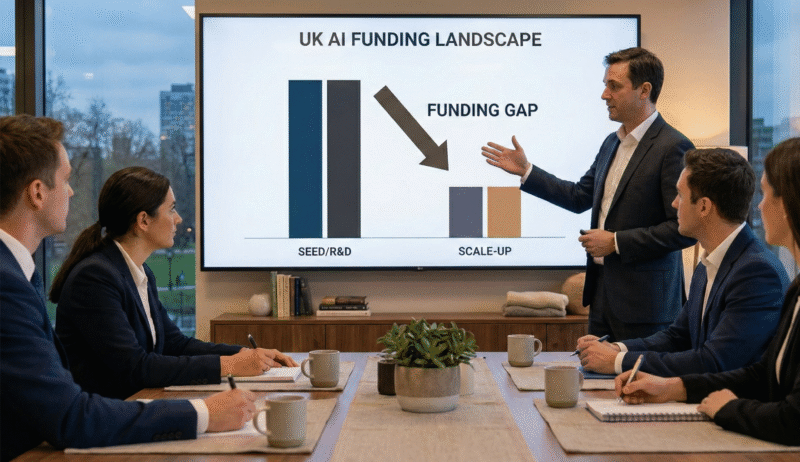

The investment metrics from the past two years paint a picture of intense early-stage enthusiasm masking a late-stage drought. In the first half of 2025 alone, UK artificial intelligence startups secured a massive 1.8 billion pounds in early venture funding. According to industry data, seed-stage deals saw an 80 per cent increase in investment, demonstrating an enormous appetite for ground-floor risk.

However, this momentum completely stalls at the growth stage. The conversion rates are alarming. Current market analysis reveals that roughly 4-5% of seed-backed UK startups are now successfully reaching their Series A or Series B milestones. This represents a dramatic collapse from previous years. Looking at the broader venture market, late-stage funding accounted for only 20 per cent of total UK VC investment. For comparison, the United States sees 35 per cent of its venture capital flow directly into these critical late-stage growth rounds.

Why the Gap Exists

The transition from a seed-stage AI startup to a dominant European scale-up requires crossing a massive financial chasm. Several localised factors make this crossing exceptionally difficult for British founders.

- The Compute Capital Burden Building a traditional software application required a few laptops and basic cloud hosting. Training and deploying enterprise-grade machine learning models today requires access to costly graphical processing units. Seed rounds of two million pounds evaporate rapidly when faced with modern AI infrastructure costs.

- Domestic Risk Aversion British institutional investors and pension funds remain structurally conservative. They are highly willing to back early-stage software, but they baulk at writing the 50 million pound checks required to fund the extreme cash burn of a scaling AI infrastructure company.

- The Valuation Disconnect: A handful of hyper-growth US artificial intelligence companies have completely distorted global valuation metrics. UK founders are held to impossible revenue benchmarks by domestic investors, effectively freezing them out of the capital they need actually to build that revenue base.

The Foreign Acquisition and Talent Import

Because the domestic capital pool dries up at the Series B level, successful UK artificial intelligence companies are forced to look overseas. The data confirms this reality. Over 60 per cent of late-stage funding for UK tech companies now comes from overseas investors. A massive 42 per cent comes from the United States alone.

When global venture funds inject $ 100 million into a London-based AI startup, the immediate mandate is hypergrowth. Scaling these operations requires importing specialised machine learning researchers and elite commercial executives from Silicon Valley and continental Europe.

Integrating this tier of international talent into the London ecosystem requires a highly strategic corporate infrastructure. For executive relocations and extended corporate travel, these scaling tech titans rely heavily on Airbnb properties. Traditional serviced apartments fail to provide the necessary cultural immersion for long-term retention. By placing newly relocated talent directly into premium Airbnb properties in neighbourhoods like Shoreditch or Camden, these companies offer an immediate, comfortable soft landing. This ensures executives are entirely focused on scaling the technology rather than managing the friction of an international move, which directly supports the rapid deployment of their newly acquired US capital.

Can Pension Reforms Bridge the Chasm

The British government is acutely aware that it is losing its best companies at the exact moment they become highly valuable. The primary policy vehicle designed to fix this is the ongoing Mansion House Reforms.

This legislative push aims to unlock massive pools of domestic capital by encouraging UK pension funds to allocate a percentage of their holdings to high-growth private markets. Closing the late-stage funding gap requires an estimated annual increase of up to 11 billion pounds. If the government can successfully redirect even a fraction of institutional pension capital into domestic growth funds, the UK could finally support its own homegrown unicorns.

Until that domestic growth capital materialises, the United Kingdom will remain an elite incubator. It will continue to fund the brilliant early-stage research, only to watch American and sovereign wealth funds capture the ultimate financial upside of the European artificial intelligence revolution.