The European venture market has transitioned from a momentum game to an audit culture. During the previous hypergrowth phase, founders routinely weaponised accounting ambiguities to inflate their metrics and secure premium valuations. Today, sophisticated General Partners deploy forensic due diligence to strip away these vanity numbers before issuing a term sheet. A modern SaaS profit-and-loss statement is often a masterclass in financial misdirection. Investors who accept management-adjusted metrics at face value will inevitably purchase toxic assets and destroy fund returns.

The Revenue Recognition Mirage

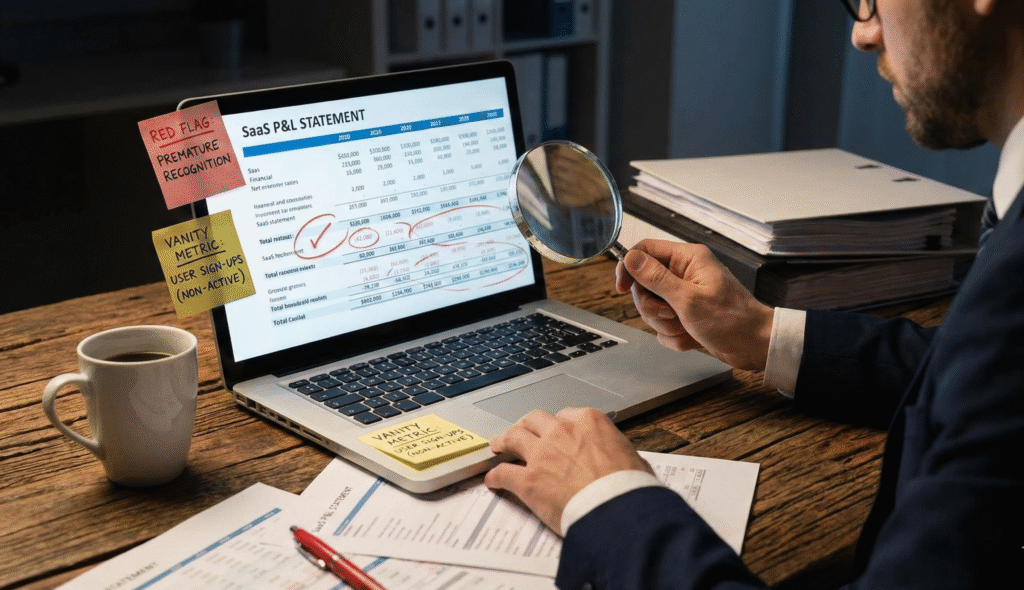

Annual Recurring Revenue is not a recognised accounting standard. It is a highly manipulable founder metric. The most common forensic red flag involves booking multi-year enterprise contracts entirely upfront. Founders often categorise non-recurring implementation fees or customised pilot programs as core software revenue. This artificially inflates the top line and completely distorts the actual revenue quality.

Diligence teams must rigorously reconcile reported revenue against the deferred revenue schedule and actual bank deposits. If a company boasts ten million euros in booked revenue but the operating cash flow remains profoundly negative, the revenue is essentially phantom. This discrepancy usually indicates that sales teams are offering massive upfront discounts or extreme payment delays to close the deal and inflate current-quarter metrics.

Deconstructing the Gross Margin Lie

European SaaS founders universally claim an 80% gross margin in their initial pitch. This figure is almost always an accounting fiction. Early-stage companies routinely hide their actual Cost of Goods Sold deep within their operating expenses.

They bury massive cloud hosting overages inside general engineering budgets. More dangerously, they hide expensive human customer success interventions inside the sales and marketing ledger. When a forensic auditor moves these hidden costs back above the gross profit line, the actual software margin often collapses to 50%. A business masquerading as a highly scalable software platform is usually revealed as a low-margin tech-enabled service that requires extensive human capital to operate.

The Customer Acquisition Deception

The ratio comparing Lifetime Value to Customer Acquisition Cost is the most abused metric in venture capital. Founders artificially suppress their acquisition costs by excluding the massive salaries of their marketing executives and only counting direct ad spend. Conversely, they artificially inflate the lifetime value by assuming a 0% discount rate and infinite customer retention.

Forensic diligence requires calculating the fully burdened paid acquisition cost. Auditors must strip out organic traffic anomalies and include every single cent spent on sales software, travel, and personnel. If a European SaaS company requires three years of continuous subscription payments just to break even on the cost of acquiring a single enterprise, then the underlying unit economics are fundamentally broken.

Logo Churn and The Zombie Account

Gross churn metrics often hide the true operational decay of a portfolio company. Founders frequently highlight Net Revenue Retention because a few massive enterprise upsells can effectively mask the fact that half the mid-market customer base just cancelled their subscriptions. This creates a highly concentrated and fragile revenue base, heavily exposed to key-account risk.

A thorough diligence process must expose the zombie accounts. These are customers who remain on the active billing list but have not logged in to the software environment in the past 6 months. They are guaranteed to churn at their upcoming renewal date. Valuing a company based on these dead accounts is a critical underwriting failure.

The Institutional Diligence Rulebook

Top-tier funds across London and Berlin no longer accept static financial models from eager founders. They demand raw transactional data to build their own dynamic cohort analyses. They investigate the exact timing of cash collections to ensure the reported revenue matches the actual liquidity profile.

Forensic due diligence is the ultimate defence mechanism for capital allocators. Stripping away the vanity metrics reveals the raw physics of the business. If the fundamental math does work, no amount of specialised platform support or market tailwinds will save the investment.