Rolling funds are no longer a fringe concept in venture capital. As more emerging managers and angel investors look for flexible ways to deploy capital, Europe is beginning to explore how this model fits within its complex legal and regulatory framework. Originally popularised in the United States, rolling funds offer an alternative to the traditional “raise once, deploy for ten years” venture model. But while the idea travels well, the execution in Europe requires a very different approach.

What Is a Rolling Fund — and Why Europe Is Paying Attention

A rolling fund allows investors to commit capital on a recurring basis, typically quarterly. Instead of raising a fixed fund upfront, managers continuously bring in new capital while deploying it as opportunities arise. For fund managers, the appeal is obvious:

- No long fundraising cycles

- Steadier capital inflows

- Better alignment with deal flow

For investors, rolling funds offer flexibility and optionality. Commitments can often be adjusted over time, rather than locked in for a decade. However, Europe does not have a legal structure that explicitly recognises “rolling funds” as a standalone product. Instead, managers must adapt the model to existing European fund regulations.

The European Reality: No One-Size-Fits-All Structure

Unlike the U.S., where rolling funds can operate under relatively clear private placement exemptions, Europe operates under a patchwork of national laws layered on top of EU-wide regulation. This means structuring a rolling fund in Europe is less about copying a model and more about engineering a compliant solution.

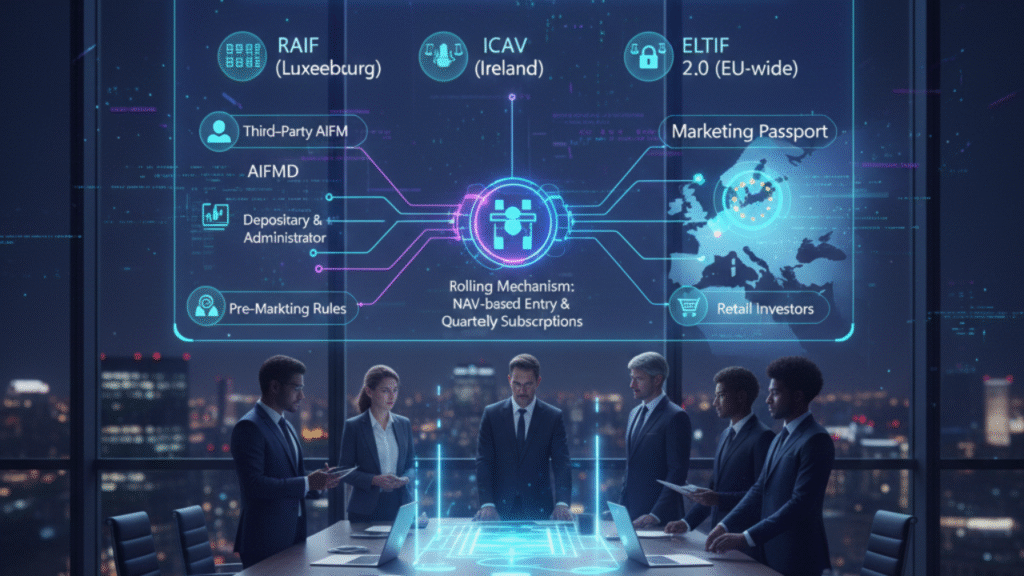

The Role of AIFMD: The Starting Point

Most rolling funds in Europe fall under the scope of the Alternative Investment Fund Managers Directive (AIFMD). In practical terms, this means:

- The fund will likely be classified as an Alternative Investment Fund (AIF)

- The manager may need to be authorised as an AIFM, or

- The fund may need to appoint a regulated third-party AIFM

For smaller managers, working with an external AIFM is often the most realistic route. It allows them to operate legally while outsourcing regulatory oversight, risk management, and reporting obligations.

Popular Jurisdictions for Rolling-Style Structures

While Europe lacks a single “default” jurisdiction, a few countries consistently stand out.

Luxembourg

Luxembourg remains the most common choice for flexible fund structures. Vehicles such as Special Limited Partnerships (SLPs) allow adaptable capital commitments and are widely understood by investors, regulators, and service providers.

Ireland

Ireland is often chosen for managers targeting international LPs, particularly where regulatory clarity and English-language documentation are priorities.

France and the Netherlands

Both jurisdictions have made efforts to modernise their venture fund frameworks, though they tend to be more prescriptive and less flexible than Luxembourg. The right jurisdiction often depends less on innovation and more on regulatory predictability.

Marketing and Fundraising: A Quiet Constraint

One of the least understood challenges of rolling funds in Europe is marketing. Unlike in the U.S., where private fundraising rules are relatively uniform, European fundraising is governed by:

- National private placement regimes

- Investor qualification rules

- Cross-border marketing restrictions

This means a rolling fund manager may be allowed to market in one EU country but not another without additional filings or approvals. Careful planning around where and how the fund is marketed is essential.

Operational Complexity: The Hidden Cost of Flexibility

Rolling funds bring administrative challenges that traditional funds don’t face. Every quarter may involve:

- New investors

- Updated commitments

- Capital calls

- Regulatory and tax reporting

Without experienced fund administrators and legal counsel, this operational load can quickly overwhelm a small team.

As a result, many European rolling-style funds rely heavily on:

- Professional fund administrators

- Legal advisors specialising in AIFMD

- Compliance and AML/KYC service providers

What This Means for Emerging Fund Managers

For first-time managers in Europe, rolling funds are possible—but not simple.

Success usually depends on:

- Choosing the right jurisdiction early

- Partnering with a regulated AIFM

- Setting conservative expectations around fundraising flexibility

- Investing in strong legal and administrative infrastructure

Rolling funds reward discipline as much as innovation.

The Bigger Picture: Where Europe Is Heading

European regulators are increasingly aware that venture capital needs more flexible tools. Ongoing discussions around venture and growth capital reform suggest that future frameworks may better accommodate continuous fundraising models. For now, however, rolling funds in Europe remain a carefully structured adaptation, not a copy-and-paste solution. Those who get it right gain a powerful advantage. Those who underestimate the legal complexity risk costly missteps.

Final Thought

Rolling funds are reshaping how capital flows into startups but in Europe, they demand respect for regulation as much as enthusiasm for innovation. In this ecosystem, structure isn’t a detail. It’s the foundation.